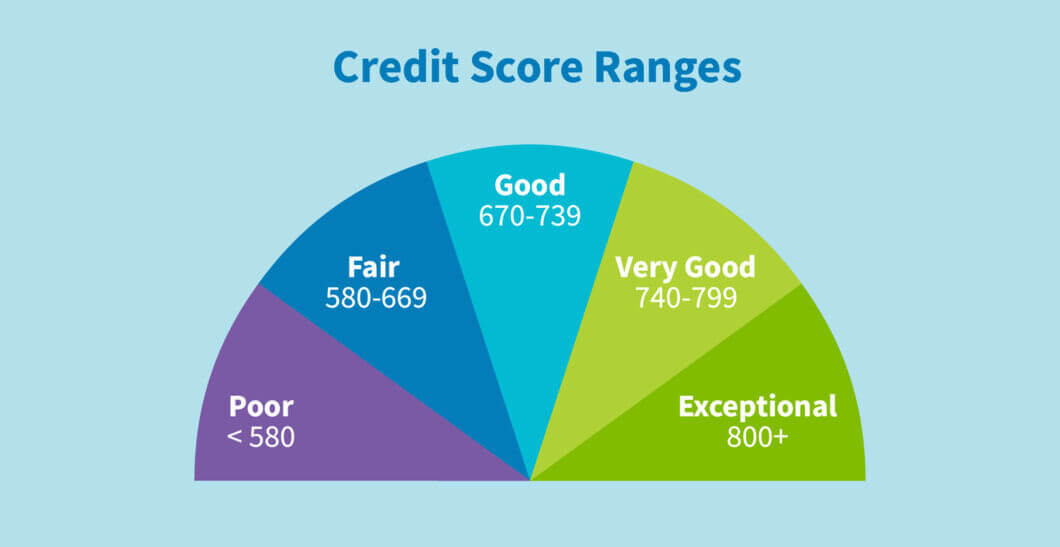

Your credit score is a number that ranges from 300 to 850 and is based on your credit history. It plays a crucial role in your financial life as it determines whether you qualify for loans, credit cards, and other financial products. A higher credit score can lead to better interest rates and lower fees, while a lower score can result in higher interest rates and reduced access to credit.

In this article, we’ll discuss why your credit score matters more than you think and provide tips for boosting your score.

Why Your Credit Score Matters More Than You Think

- It determines your ability to access credit: Your credit score is a reflection of your creditworthiness. Lenders use your credit score to assess your risk level and determine whether to approve your credit application or not. A low credit score indicates a high risk of default, which makes lenders less likely to approve your application.

- It affects the interest rates you receive: Your credit score also plays a significant role in the interest rates you receive on loans and credit cards. A higher credit score typically leads to lower interest rates, while a lower score results in higher interest rates. Over time, even a small difference in interest rates can translate into thousands of dollars in savings or additional costs.

- It impacts your insurance rates: Many insurance companies use your credit score to determine your insurance rates. Studies have shown that people with lower credit scores tend to file more insurance claims, which makes them a higher risk for insurance companies. As a result, they may charge higher premiums or deny coverage altogether.

- It affects your job prospects: Some employers use your credit score as part of their hiring process. While they cannot use your credit score to determine your eligibility for a job, they can use it to assess your financial responsibility. A low credit score may raise red flags for some employers, making it more difficult to secure employment.

Also Read: Financial Mistakes You Need to Avoid

Tips for Boosting Your Credit Score

- Pay your bills on time: Payment history is the most significant factor that affects your credit score. Late payments can have a severe impact on your score, so it’s essential to make your payments on time.

- Keep your credit utilization low: Credit utilization refers to the amount of credit you’re using compared to your credit limit. High credit utilization can hurt your credit score, so it’s best to keep it below 30%.

- Monitor your credit report: Your credit report contains information about your credit history, including your credit score. It’s essential to review your credit report regularly to ensure that the information is accurate and up-to-date. If you notice any errors, dispute them immediately.

- Avoid opening too many new accounts: Opening too many new credit accounts in a short period can hurt your credit score. Each time you apply for credit, it results in a hard inquiry on your credit report, which can lower your score.

- Use credit responsibly: Using credit responsibly means using it only when necessary and paying it off in full each month. This behavior demonstrates financial responsibility and can help boost your credit score over time.

Also Read: Ways to Save Money and Improve Your Finances

FAQs

- How long does it take to improve my credit score?

Improving your credit score takes time and effort. It’s not something that can be done overnight. However, by following the tips outlined in this article, you can start to see improvements in your score within a few months.

- Can I improve my credit score if I have negative information on my credit report?

Yes, you can still improve your credit score, even if you have negative information on your credit report. The negative information, such as late payments, collections, or bankruptcies, may stay on your credit report for up to seven years. However, its impact on your credit score lessens over time, especially if you have positive information on your credit report, such as on-time payments and low credit utilization.

- How often should I check my credit score?

You should check your credit score at least once a year. You can request a free credit report from each of the three major credit bureaus – Equifax, Experian, and TransUnion – once every 12 months. You can also use a credit monitoring service that provides regular updates on your credit score and report.

- Will checking my credit score hurt my credit?

No, checking your credit score does not hurt your credit. When you check your credit score, it results in a soft inquiry, which does not affect your credit score. However, when you apply for credit, it results in a hard inquiry, which can lower your credit score.

Conclusion

Your credit score plays a critical role in your financial life. It affects your ability to access credit, the interest rates you receive, your insurance rates, and even your job prospects. By following the tips outlined in this article, you can boost your credit score and improve your overall financial health. Remember to pay your bills on time, keep your credit utilization low, monitor your credit report, avoid opening too many new accounts, and use credit responsibly. By doing so, you can improve your credit score and open doors to better financial opportunities. So, don’t underestimate the importance of your credit score – it matters more than you think!