In the intricate world of finance, there exists a realm often spoken of in hushed tones – shadow banking. It’s a term that sounds mysterious, conjuring images of secrecy and intrigue. But what exactly is the shadow banking system, and why does it matter? Let’s delve into this financial phenomenon to unravel its complexities.

Defining the Shadow Banking System:

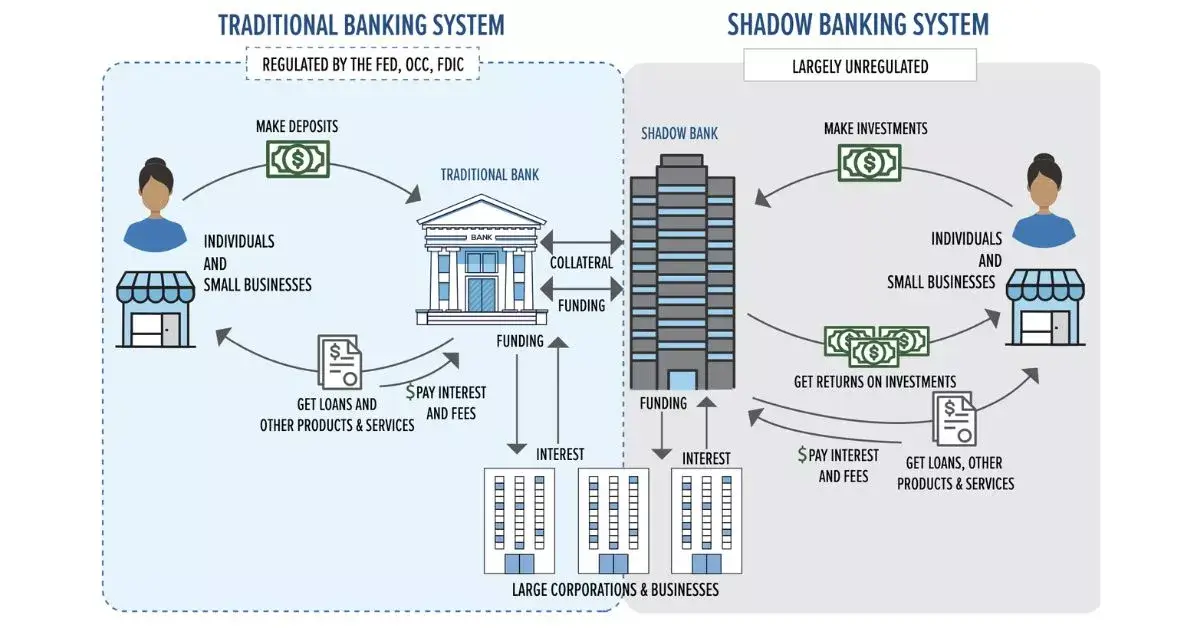

The shadow banking refers to a diverse set of financial activities and institutions that operate outside traditional banking regulations. These include hedge funds, money market funds, non-bank financial institutions, and more. Unlike traditional banks, they don’t hold banking licenses and often operate in the shadows of the formal banking sector.

Key Components:

- Money Market Funds: These are mutual funds that invest in short-term debt instruments. They are a significant part of the shadow banking, offering short-term financing to various entities.

- Securitization: The process of bundling loans into securities that can be sold to investors. Mortgage-backed securities are a classic example.

- Hedge Funds: Investment funds that employ various strategies to generate high returns. They often engage in complex and high-risk transactions.

Shadow Banking System’s Role in the Economy:

The shadow banking system plays a vital role in providing credit to the economy. It often serves borrowers who might not qualify for loans from traditional banks. By diversifying the sources of credit, it contributes to financial innovation and can enhance market liquidity.

Regulatory Challenges:

One of the primary concerns with the shadow banking is its lack of regulation compared to traditional banks. This lack of oversight can pose systemic risks, as was evident during the 2008 financial crisis when certain shadow banking activities amplified the impact of the crisis.

Impact on Global Financial Stability:

While the shadow banking fosters financial innovation, its rapid growth can create vulnerabilities. If not properly managed, these vulnerabilities can lead to financial contagion, affecting not only specific institutions but the entire global financial system.

Current Regulatory Efforts:

In the aftermath of the 2008 financial crisis, regulatory bodies across the world intensified efforts to bring the shadow banking system under tighter supervision. Stricter regulations aim to mitigate risks and enhance transparency, ensuring a more stable financial environment.

The Future of Shadow Banking:

As financial landscapes continue to evolve, so will the shadow banking system. The key lies in balancing innovation and regulation. Striking this balance will be crucial in harnessing the benefits of the shadow banking while mitigating potential risks.

What are the risks of the shadow banking system?

The shadow banking system poses a number of risks to the financial system, including:

- Procyclicality: The shadow banking can amplify the boom-bust cycle in the economy. When the economy is doing well, the shadow banking system can create a lot of credit, which can lead to asset bubbles. When the economy turns down, these bubbles can burst, leading to a sharp decline in asset prices and a credit crunch.

- Interconnectedness: The shadow banking is highly interconnected with the traditional banking system. This means that problems in the shadow banking system can quickly spread to the traditional banking system, and vice versa.

- Lack of transparency: The shadow banking is less transparent than the traditional banking system. This makes it difficult to assess the risks posed by the shadow banking and to identify potential problems.

How is the shadow banking system regulated?

The shadow banking system is less regulated than the traditional banking system. This is because shadow banking institutions are not subject to the same capital requirements and other regulations as traditional banks. However, in recent years, regulators have taken steps to increase oversight of the shadow banking system.

For example, the Dodd-Frank Wall Street Reform and Consumer Protection Act, which was passed in the wake of the 2008 financial crisis, created the Financial Stability Oversight Council (FSOC). The FSOC is responsible for identifying and responding to systemic risks to the financial system. The FSOC has the power to designate non-bank financial institutions as systemically important financial institutions (SIFIs). SIFIs are subject to stricter regulation than other non-bank financial institutions.

Banking in the Digital Age: How Technology is Transforming the Financial Landscape

What role did the shadow banking system play in the 2008 financial crisis?

The shadow banking system played a significant role in the 2008 financial crisis. Shadow banking institutions were involved in a number of risky activities, such as securitizing subprime mortgages and creating synthetic CDOs. These activities contributed to the formation of the asset bubble that led to the crisis.

For example, hedge funds and private equity firms were heavily involved in the securitization market. Securitization is the process of bundling together loans and other assets and selling them to investors as securities. Securitization can be a useful tool for spreading risk, but it can also be used to create risky securities. In the lead-up to the crisis, hedge funds and private equity firms securitized billions of dollars of subprime mortgages. These securities were often sold to investors with little understanding of the risks involved.

What are some examples of shadow banking institutions?

Examples of shadow banking institutions include:

- Hedge funds

- Private equity firms

- Structured investment vehicles (SIVs)

- Money market funds

- Asset-backed commercial paper (ABCP) conduits

- Repurchase agreement (repo) markets

More post that you might like to read-

- Yellen to Push for World Bank Reforms and Engage with China at Global Meetings.

- Decoding World of Investment Banking: Unraveling Opportunities, Strategies, and Success.

What are the arguments for and against regulating the shadow banking system?

Proponents of regulating the shadow banking system argue that it is necessary to reduce the risks posed by the shadow banking system to the financial system. They also argue that regulation would help to level the playing field between shadow banking institutions and traditional banks.

Opponents of regulating the shadow banking system argue that it would stifle innovation and make it more difficult for businesses to access credit. They also argue that regulation would be difficult and costly to implement.

The debate over regulating the shadow banking system is likely to continue for some time. There are strong arguments on both sides of the debate. Ultimately, it is up to policymakers to decide how to best regulate the shadow banking system in order to reduce the risks it poses to the financial system.

In addition to the risks listed above, the shadow banking system can also contribute to financial inequality. Shadow banking institutions often cater to wealthy investors and businesses, while traditional banks are more likely to serve middle-class and low-income borrowers. This means that the shadow banking system can help to widen the gap between the rich and the poor.

Final words

The shadow banking system is a complex and integral part of the global financial network. Its role in providing credit and fostering financial innovation cannot be undermined. However, it demands careful regulation and scrutiny to prevent systemic risks. As we navigate the intricacies of modern finance, understanding the shadow banking system becomes essential, empowering us to advocate for responsible financial practices and a stable economic future.