Why Your Credit Score Matters More Than You Think: Tips for Boosting Your Score!

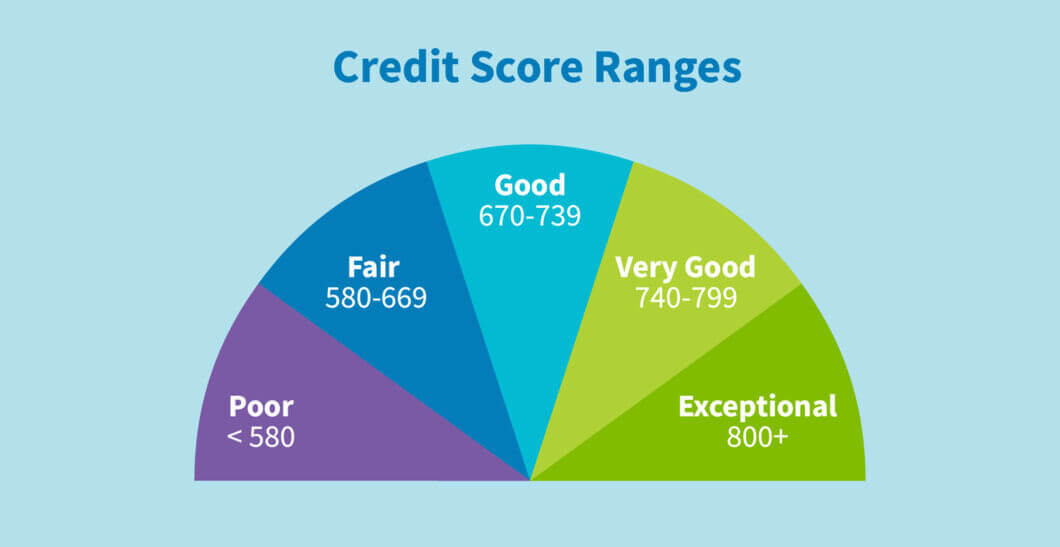

Your credit score is a number that ranges from 300 to 850 and is based on your credit history. It plays a crucial role in your financial life as it determines whether you qualify for loans, credit cards, and other financial products. A higher credit score can lead to better interest rates and lower fees, … Read more